Lure of real estate fades as overseas capital seeks better bargains, Hu Yuanyuan reports from Beijing.

|

|

A migrant worker passes a poster for housing developments in Shaoyang, Hunan province. The country's economic growth slowed last year due to tight control of the property market and a recession in world business. Lu Jianshe / for China Daily |

It's a frustrating time for overseas investors in Chinese real estate, especially those looking to turn a quick profit.

One potential investor, a managing director in Hong Kong for a leading US fund, looked into many real estate projects in China last year but did not sign any deals.

Instead, he sold a number of big projects ahead of pre-set investment deadlines.

He requested anonymity because of company policy against speaking to the media. But he was clear about his exasperation at not being able to achieve his objectives.

"Despite the ongoing correction in China's property market, investment opportunities are not as competitive as the EU and US," he said.

All investment decisions for his global real estate fund are made by its New York office.

"We have to compete with other teams in the EU and US where there are more bargains because of the recession," he said.

"Our investment in China, in fact, is more on the long-term perspective and for risk diversification in our global investment portfolio."

|

|

Significant outflow

His case is quite representative. John Wong, director of investment services at Colliers International (Beijing), a real estate consultancy, said that overall, more international real estate capital was withdrawn from China than came in last year.

In Beijing, for instance, approximately 10 en bloc sales transactions were concluded and disclosed in 2011 but there was little foreign participation. Domestic investors - State-owned enterprises, financial institutions and private developers - continued to denominate the market, while overseas investors' involvement became more constrained, according to a recent report by Colliers International.

China's real estate sector and stocks are the major fields that have been favored by international hot money, the funds flowing from one country to another to earn a short-term profit. Those funds are leaving China.

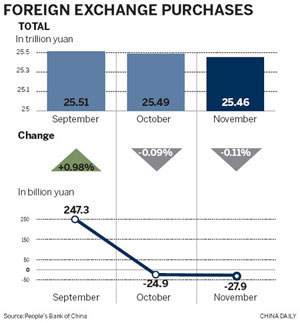

A key indicator for analysts is the amount of foreign exchange bought by Chinese banks, and the amounts declined in November for the second consecutive month. (The release of December figures is expected later this month.)

The percentage of change does not sound like much, but it is significant when the purchases in a month total hundreds of trillion yuan.

After a strong September, the value of purchases fell in October for the first time in four years - down 0.09 percent, 24.9 billion yuan. In November, purchases dropped 0.11 percent, the largest monthly decline since December 2007.

Less taste for risk

The reasons for the capital outflow, analysts said, include global investors' lessened appetite for risky assets amid the global economic recession, growing worries over a hard landing by China's economy and the yuan's recent depreciation.

Ding Zhijie, dean of the School of Banking and Finance at the University of International Finance and Economics, said the yuan's decline demonstrates the shortage of dollar liquidity.

"Since the worsening European debt crisis sent global financial markets into turmoil by the end of September, it's an obvious trend that global capital has been flowing into dollar-dominated assets," Ding said. The US dollar has been in great demand in the market, he said.

According to the State Administration of Foreign Exchange, the annual inflow of hot money to China during the past decade averaged nearly $25 million. Total accumulated inflow 2003-10 hit $300 billion, betting on appreciation of the yuan.

Most of this capital sought haven for speculative profits in the property market, the stock market and the underground banking system.

"Lower growth in Europe in the course of fiscal austerity and the banks' needs to increase capital coverage would affect East Asia," Bert Hofman, the World Bank's chief economist for East Asia and the Pacific, said in November. He said that less credit from European banks could mean reduced capital flows to the Asia-Pacific region.

Lu Zhengwei, chief economist with Industrial Bank, said investors' worries about an economic hard landing and the risks of local government debt also contributed to the outflow of hot money.

The country's economic growth slowed last year, from 9.7 percent in the first quarter to 9.5 percent in the second and 9.1 in the third. Most economists have estimated China's economy will grow 8 to 8.5 percent this year, dragged down by falling exports and investment.

|

|

China's stock market is one of the major fields that international investors have favored. Xie Zhengyi / for China Daily |

'Deflate slowly'

"Meanwhile, the impact of tightened monetary policy on the real economy and the looming turning point for the real estate market also are likely to trigger capital outflow," said Du Zhengzheng, a research analyst with China Development Bank Securities.

Hou Yunchun, deputy director of the Development Research Center of the State Council, said the property market will pose the biggest challenge for China's economy this year. "The property bubble should be deflated slowly and not pricked," he said.

The government's continual measures to cool the real estate market - including increasing the down payment required and limiting the number of homes a family may buy - are working, which means they have begun to bite the real estate market.

In November, 49 of 70 monitored cities reported that prices for newly built residential properties fell from a month earlier, while prices in 16 cities remained unchanged, according to figures released by the National Bureau of Statistics.

"We expect that property investment, home sales, the floor space in new projects and land sales will all decline in the first quarter of 2012, and the correction in the real estate market will be the largest uncertainty facing the economy this year," said Gao Ting, chief China strategist at investment bank UBS AG.

RMB vs dollar

Bigger fluctuation in the renminbi is another reason for the capital outflow. In November, the yuan weakened for 12 consecutive trading days and once triggered concerns that the Chinese currency might head toward a devaluation cycle.

Zhao Qingming, a senior researcher with China Construction Bank, the country's second largest lender by market value, said a stronger yuan in 2011 was near the lower end of what he once predicted would be an appreciation of 5 and 7 percent. He expects to see bigger fluctuations against the US dollar ahead.

The accelerating withdrawal of hot money, experts said, will impose more pressure on the yuan's depreciation and will trigger bigger fluctuations in the country's stock and bond markets as well as the property sector.

"However, such an outflow is not likely to deliver a big shock to the real economy due to China's strict management of the capital account and the scale of the economy and foreign exchange reserves," said Fan Jianjun, an economist with the State Council Development Research Center.

But if the trend of capital outflows continued, analysts said, China might return to a dollar peg, as it did during the world financial crisis in 2008.

Instead of allowing for the yuan's steady depreciation, the central bank has set the middle trading price of the yuan at a persistently high level. The aim is to stabilize the yuan's value against the dollar as investors sell the currency on expectations that it will further depreciate.

"If such exchange-rate stability fails to change market expectations of a weakening yuan, it will cause more capital outflows and the situation won't ease at least until the first quarter of this year," said Industrial Bank's Lu.

According to Zhang Zhiwei, chief China economist at Nomura International, the increasing capital outflows also reflect China's shrinking trade surplus and slowing foreign direct investment in the short run.

As Chang Jian, economist with Barclays Capital, wrote in a recent research note, "Capital outflows, together with a narrower trade surplus and slowing FDI, are likely to reduce appreciation expectations and reinforce depreciation expectations, given a weakening global economy and investor sentiment."

The upside

The outflow of hot money is not all bad, however. Deprecation of RMB will give exporters a more competitive edge if, as expected, external demand plunges amid the global economic slowdown.

On the monetary policy side, it provided more leeway for the central bank to fine-tune its policy to deal with the domestic economic slowdown.

For Zhang, the capital outflow could prompt the People's Bank of China to cut the reserve requirement ratio again to offset the recent decline of foreign-exchange purchases. In December, the central bank lowered the ratio for commercial lenders for the first time since December 2008.

Zhang forecast that the central bank would soon cut the ratio by 50 more basis points and loosen requirements for banks' loan-to-deposit ratios to stabilize domestic liquidity.

For Zhou Jingtong, a researcher with the Bank of China, the outflow of foreign capital is not a major concern because "it is not a long-term trend". Zhou said the outflow will be corrected because the yuan will appreciate against a weakening US dollar in the long run.

Yi Xianrong, a researcher with the Institute of Finance and Banking under the Chinese Academy of Social Sciences, said that instead of focusing on the retreat of foreign capital, the government should pay special attention to the possible accelerated outflow of homegrown funds. That, Yi said, is expected to have larger repercussions for domestic monetary policy.

Chen Keyu contributed. Write the reporter at [email protected].

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 130349 ![]()