China's move to lower merchant fees for bankcards would be credit negative for banks, said the Moody's Investors Service in a report released on Monday.

"We estimate that for the commercial banks we rate, the reduction in merchant fees would reduce their merchant fee income by nearly 30 percent and cause aggregate pre-tax profit to decline by 1 to 1.5 percent," said Katie Chen, an associate analyst at Moody's Investors Service Hong Kong Ltd.

Last week Xinhua News Agency reported that the central bank circulated a notice earlier in the month stating that the State Council had approved lower merchant fees for bankcard transactions, effective from Feb 25.

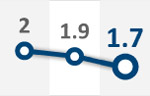

Bankcard merchant fees would be 1.25 percent for entertainment-related purchases, 0.38 percent for purchases related to daily living and 0.78 percent for other types of purchases.

Although the card business is a minor contributor to income and profits, lower merchant fees will undermine a promising channel for banks to grow their fee-based income, Chen said.

"Without the increase in bankcard fee income, these banks' total fee and commission income would have risen only 0.4 percent because other fees, such as those related to consultancy and advisory services and lending, declined."

During the first half of 2012, bankcard fee income surged 36 percent year-on-year for the Chinese banks rated by Moody's, while total fee and commission income grew 6 percent, said the rating agency.

At present, the merchant fees that banks and merchants negotiate average 1 to 2 percent depending on the type of purchases, including service fees charged by the banks issuing the cards, clearing institutions such as UnionPay, VISA, or MasterCard, and the banks handling the payment for the merchants.

The fee reduction threatens to increase the risks within banks' credit card loan portfolios in a number of ways, according to Chen, as banks may try to accelerate volume growth to make up for the loss in fee income.

"Using the entertainment segment as an example, the reduction of merchant fees to 1.25 percent from 2 percent implies that banks would need a 60 percent jump in transaction volume just to maintain current income. This is far higher than the 36.6 percent growth recorded in the third quarter and raises the risk that banks will adopt more aggressive competitive strategies, including lowering their underwriting and card issuance standards, to expand their volume."

Another risk is that banks may attempt to increase their bankcard fee income by promoting the usage of their cards for overdrafts or installment payments, according to the report.

The fee reduction will have a greater effect on joint stock commercial banks, whose revenue contribution from bankcards is higher. Such banks include China Guangfa Bank, Ping An Bank, China Everbright Bank, Bank of Communications and China Merchants Bank, it said.

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()